In many technology organizations, testing is viewed primarily as an engineering responsibility. Engineers write unit tests, QA teams run test suites, and automation frameworks verify that APIs and services behave as expected. Once those tests pass, a feature is often considered ready for release.

For many types of software, this model works well. Engineering ensures the code behaves according to specification, and QA validates the implementation under various scenarios. The boundaries between responsibilities are relatively clear.

Fintech products, however, operate under a different set of constraints.

Financial systems are long-lived, highly regulated, and deeply interconnected. They operate across multiple systems and must remain accurate over months or even years of customer activity.

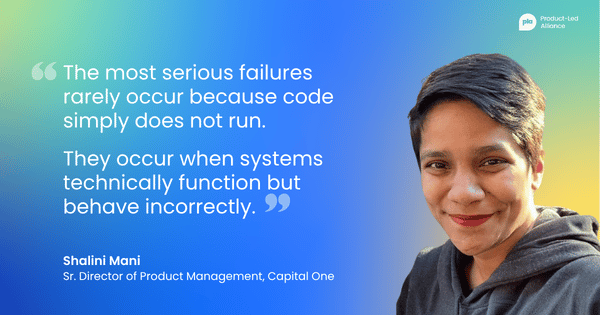

In this environment, the most serious failures rarely occur because code simply does not run. Instead, they occur when systems technically function but behave incorrectly within the broader lifecycle of the product.

That distinction is important. A system can pass every engineering test and still produce outcomes that confuse customers, violate product expectations, or create operational incidents. This is where product thinking becomes essential.

Code correctness versus product correctness

Engineering tests focus primarily on validating that the system performs the logic it was designed to execute. For example, engineers may verify that a payment API successfully processes transactions, that the database stores the correct values, or that the billing service calculates interest using the configured formula.These are critical validations, and without them, systems would fail quickly and visibly.

However, they answer only part of the question.

Product correctness asks whether the system is behaving appropriately within the real-world context of the financial product. Consider a simple payment scenario. The payment may be processed successfully by the API and correctly recorded in the database, yet still create an incorrect outcome for the customer depending on how it interacts with billing cycles, promotional interest periods, or dispute protections.

In these situations, nothing is technically broken. The code performed exactly as written. The issue lies in the underlying product logic and how different rules interact over time.

Financial systems are full of these interactions. Whether a payment applies to the current billing cycle or the previous one can change how interest accrues. Whether a promotional rate expires before or after a payment is posted can change the customer’s balance. Whether a dispute is active can determine whether certain fees should apply.

Testing these behaviors requires more than validating individual components. It requires understanding how the product behaves across its lifecycle.

Why fintech products are inherently difficult to test

Testing becomes particularly challenging in fintech because financial products operate across several dimensions simultaneously.

1. Long product lifecycles

First, financial products have long lifecycles. A credit card account or loan may remain active for years. During that time, the account moves through many stages: application, approval, activation, billing cycles, payments, delinquency management and eventually closure. Each stage changes how the system behaves.

A feature that works perfectly during normal account activity may behave very differently once the account enters delinquency or dispute resolution.

2. Complex calculations

Second, financial systems involve complex calculations. Interest accrual, fees, rewards programs and amortization schedules all depend on detailed rule configurations. Even small changes in timing or ordering can produce different financial outcomes. A payment applied before interest accrual may generate a different balance than one applied afterward.

If testing focuses only on the calculation engine rather than the surrounding lifecycle logic, these differences may not become visible until customers see incorrect balances.

3. Strict regulatory requirements

Third, fintech systems must satisfy strict regulatory requirements. Many regulations specify behaviors that depend on the state of the account. Certain disclosures must be delivered when an account becomes delinquent. Dispute processes follow defined timelines. Billing statements must reflect precise calculations.

Testing must therefore validate not only functional behavior but also compliance with these obligations across multiple lifecycle states.

4. External dependencies

Finally, fintech systems rarely operate in isolation. They rely on payment processors, fraud detection systems, credit bureaus, identity verification services, and numerous internal platforms.

Failures often occur not because a system behaves incorrectly on its own, but because it behaves correctly while another system behaves unexpectedly. A processor might send duplicate confirmations, or a fraud system might temporarily block legitimate activity. Testing must anticipate how the product behaves when these external dependencies produce unusual responses.

Where product managers contribute the most

Product managers are uniquely positioned to strengthen testing in these environments because they often understand the full context of how financial workflows operate.

While engineers may focus on implementing individual services, product managers tend to see how the system behaves across the broader lifecycle of the product. This perspective helps identify scenarios that might otherwise be overlooked during testing.

One important area is identifying lifecycle edge cases. Customers rarely follow idealized workflows. They make partial payments, open disputes while billing cycles are active, update account settings mid-transaction, or complete applications across multiple sessions. These behaviors can produce combinations of events that do not appear in technical specifications but occur frequently in production environments.

Product managers also help identify interactions between product rules. Financial products often involve overlapping rules such as promotional interest periods, payment allocation priorities, fee structures, and dispute protections. Testing each rule individually is not sufficient. The most complex scenarios occur when multiple rules interact at the same time.

Operational awareness also plays an important role. Product managers typically interact with support teams, risk teams, and operations teams that manage manual reviews and exception handling. These operational realities often reveal scenarios that pure feature testing might miss. For example, what happens if identity verification fails and the application must enter manual review? What happens if a system outage interrupts a billing process?

These situations are not unusual; they’re part of everyday operations in financial systems.

What happens when product thinking is missing

When testing focuses only on technical correctness, several categories of problems tend to emerge.

One common issue is lifecycle inconsistency. A feature may function correctly for active accounts but behave unexpectedly when the account enters another lifecycle stage, such as delinquency or dispute resolution.

Another issue involves integration surprises. Systems may behave correctly internally but produce unexpected outcomes when interacting with external dependencies. A processor might return responses in an unexpected order, or a fraud service might temporarily block transactions. Without product-level testing scenarios, these interactions may not be fully examined.

Perhaps the most visible failures occur when the customer experience does not accurately reflect the true system state. A customer might see a generic message such as “processing” while the system is actually waiting for documentation or external verification. These mismatches between system behavior and user communication often erode trust more quickly than technical failures.

A practical testing lens for product teams

Product managers do not need to write automated tests to contribute meaningfully to testing. Instead, their role is to help shape the scenarios that teams test.

One helpful approach is to evaluate testing through four lenses.

- Lifecycle test: Examine how features behave across different stages of the product lifecycle.

- Edge-case test: Explore unusual but realistic customer behaviors.

- Integration test: Consider how the system responds when external services behave unexpectedly.

- Operational test: Evaluate how processes behave when delays, outages, or manual reviews occur.

By asking these questions early, product teams can ensure that testing reflects real-world complexity rather than simplified workflows.

Testing the product, not just the code

Testing in fintech is not simply about verifying whether code runs successfully. It’s about verifying whether the product behaves correctly within the complex environment in which financial systems operate.

That environment includes regulatory requirements, lifecycle transitions, customer behavior, and interactions across multiple systems.

Engineering and QA teams play a critical role in validating system stability and correctness. Product leaders complement that work by ensuring that the scenarios being tested reflect how the product actually behaves in the real world.

When those perspectives come together, testing becomes more than a technical safeguard. It becomes a way of protecting the integrity of the product itself – and in financial services, that integrity is what ultimately protects customer trust.

Become a PLA Insider

Thank you for subscribing

Get exclusive insights, frameworks, and strategies from product leaders driving real business impact.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn