In banking, we often talk about products as if they’re defined by what the customer sees: the app, the interface, the latest feature shipped. Screenshots become proxies for progress. Roadmaps fill with UI changes. Success is measured in releases.

But this framing misses a fundamental truth. In financial services, the interface is not the product. It’s a window into something far more consequential. The real product is the system beneath the surface: the network of platforms, controls, decisions, and safeguards that move money, manage risk, and preserve trust at scale.

A banking app may feel simple and instantaneous, but every tap triggers a chain of events across multiple systems, institutions, and regulatory boundaries. What looks like a clean interaction on a screen is, in reality, a coordinated execution of some of the most complex and high‑stakes infrastructure in modern software.

In that world, the quality of the system is the customer experience.

The app: A window, not the engine

A banking app might appear simple; at the touch of a button, the user gets a result. With ease, they can:

- Check their balance

- Make a payment

- View transactions

From a user perspective, it feels instantaneous. But behind each of those actions is a chain of systems working together:

- Payment rails moving money between institutions

- Fraud detection systems evaluating risk in real time

- Compliance checks ensuring regulatory requirements are met

- Ledger systems recording the source of truth

- Reconciliation processes confirming everything balances

What the user experiences as a single interaction is the output of a complex, coordinated system. That system is the product.

The ripple effect: Why every "small" change is a system-wide event

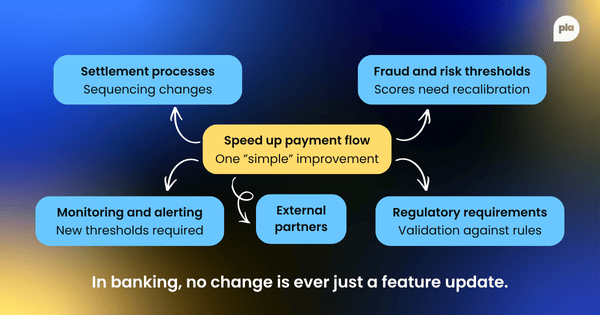

In banking, even small changes can ripple through multiple layers. A seemingly simple improvement: speeding up a payment flow, could require:

- Changes to settlement processes

- Updates to fraud and risk thresholds

- Coordination with external partners or networks

- Adjustments to monitoring and alerting systems

- Validation against regulatory requirements

What looks like a customer-facing feature update is often a broad cross-system redesign. This is why product work in banking feels different. You’re not designing screens. You’re shaping how systems interact under real-world constraints.

The illusion of slow progress: Where the real work happens

From the outside, banking product development can look slow, with fewer releases and longer timelines. But that perception misses where the most important work is happening. These changes aren't always visible to the customer but are fundamental to the product's integrity:

- Improving system resilience

- Reducing failure rates

- Strengthening fraud detection

- Handling edge cases more safely

- Making processes auditable and compliant

These changes don’t always result in new features or shiny releases, but they fundamentally improve the product. Because in banking, a product that looks good but fails under pressure is not a good product.

The high-stakes environment: The constraint of irreversible mistakes

One reason banking systems are built this way is simple: some mistakes can't easily be undone. A flawed UI that leads to a poor customer experience can be fixed. But a fraud incident or a compliance breach is much harder to reverse and has far greater implications, including loss of customer trust and regulatory scrutiny. This reality shifts the focus of product decisions:

- Speed → correctness

- Iteration → reliability

- Experimentation → controlled change

This doesn’t mean innovation is impossible. It means innovation must happen within a system that prioritizes trust and safety at scale.

Where AI fits into this

AI adds another layer to this dynamic. On the surface, AI can enhance banking products in obvious ways with smarter insights, automated support, and personalized recommendations.

But integrating AI into banking isn’t just a feature decision. It affects:

- How decisions are made (and explained)

- How risk is evaluated

- How outcomes are monitored

- How trust is maintained

An AI-powered feature isn’t just a UI improvement. It becomes part of the system, influencing decisions that may have financial, regulatory, or customer impact. This means it must be designed, governed, and integrated at a system level.

Product management as system stewardship

In this context, product management in banking is less about feature ownership and more about system stewardship. The product manager is not the CEO of a screen; they’re accountable for the health, coherence, and evolution of a living system.

This changes what “ownership” really means. A banking product manager must understand how customer journeys map onto ledger entries, how operational processes translate into system states, and how policy decisions surface as constraints in software.

Decisions are rarely isolated. Every prioritization choice, dependency trade-off, or scope decision shapes how the system behaves under stress. Change management therefore becomes a core product capability. Product managers are responsible for sequencing change in a way that the organization, its systems, and its regulators can absorb. This includes:

- Managing blast radius, not just delivery dates

- Understanding failure modes before optimising happy paths

- Planning for coexistence of old and new behaviours during transition

- Designing rollouts that preserve trust while the system evolves

In this model, the product manager acts as a translator – between customer needs and operational realities, between regulatory intent and technical implementation, and between long-term system integrity and short-term business pressure. The success of the role is not measured by how much changes, but by how safely, predictably, and sustainably change occurs.

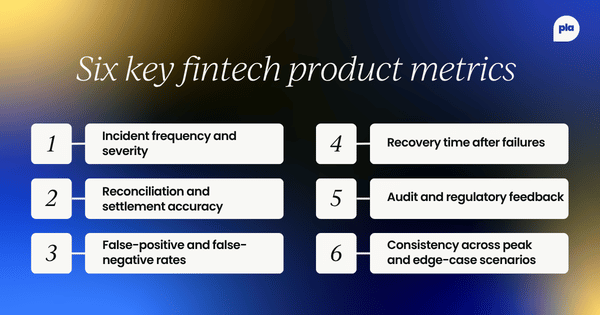

Redefining product success metrics in banking transformation

Traditional product metrics tend to reward visible progress: features launched, screens redesigned, flows simplified. But in banking, these metrics are insufficient and often misleading during periods of change.

When the real product is the system, success must be measured at the system level. Product management must elevate metrics that reflect resilience, correctness, and control, such as:

- Reduction in incident frequency and severity

- Improved reconciliation accuracy and settlement confidence

- Lower false-positive and false-negative rates in risk and fraud models

- Faster recovery times when failures occur

- Improved audit outcomes and regulatory feedback

- Predictability of outcomes across peak and edge-case scenarios

Many of these improvements are invisible to customers until they fail. Yet they’re central to long-term customer value and institutional trust. Effective product management in banking makes this invisible work legible to stakeholders, ensuring it is prioritized, funded, and protected from being crowded out by surface-level enhancements.

This redefinition of success also reshapes how change is communicated. Rather than framing progress solely in terms of what is new, product leaders must articulate what is now safer, more reliable, or more controlled. In regulated environments, confidence is built not through novelty, but through demonstrated consistency under pressure.

Ultimately, strong product management in banking transformation is about enabling change without destabilization. It ensures that evolution strengthens the system rather than fragmenting it. Preserving trust while the organization adapts to new demands, technologies, and risks.

How product teams manage change in banking systems

At a practical level, product management in banking is the discipline of turning strategic intent into safe, incremental system change. This requires specific working practices that differ from consumer-tech or startup models.

First, product discovery is inseparable from system understanding. Before defining solutions, product managers must invest in mapping:

- System dependencies and integration points

- Upstream and downstream impacts of change

- Operational processes and manual interventions

- Regulatory and control touchpoints

- Known failure modes and historical incidents

This means discovery often starts not with user interviews, but with engineers, operations, risk, compliance, and other internal teams. The goal is to understand not just what users want, but what the system can safely absorb.

Second, roadmaps are structured around risk and sequencing, not just features. Effective banking roadmaps:

- Decompose big ambitions into controllable increments

- Prioritize enablers before outcomes (e.g., data integrity before automation)

- Explicitly surface dependencies and transitional states

- Allow new and old behaviours to coexist safely during migration

Progress is measured less by delivery volume and more by reduction in uncertainty. A successful increment may simply prove the system can support a new behaviour at limited scale and that is legitimate product value.

Finally, launch is not a moment, but a managed condition. Product teams design releases with:

- Gradual rollouts and kill switches

- Enhanced monitoring and alerting

- Clear ownership for post-release behaviour

- Pre-agreed rollback and containment plans

In this model, outcomes are shaped over time, not declared at release. Product managers remain accountable after deployment, watching how the system behaves in real conditions and adjusting responsibly.

This is what change management looks like when the product is the system. It’s deliberate, cross-functional, and often invisible, but it’s precisely what allows banks to evolve without breaking the trust placed in them.

Final thought: The system is the experience

In most industries, a product that looks good but occasionally fails is inconvenient. In banking, it is unacceptable.

The true measure of a banking product is not how often it dazzles, but how consistently it performs under pressure. When volumes spike, when fraud patterns shift, when dependencies fail, when regulators ask hard questions. That is when the real product is exposed.

This is why the most important product work in banking is often invisible. It lives in resilience, correctness, auditability, and controlled change. It shows up not as a new feature, but as fewer incidents, cleaner reconciliations, safer decisions, and systems that behave predictably in uncertain conditions.

For product teams, this requires a different definition of success. Not velocity for its own sake. Not surface-level innovation. But stewardship of a complex system that people trust with their money, their livelihoods, and their confidence in the institution behind every transaction.

Because in banking, the app is only what the customer sees. The system is what the customer depends on. And that system is the real product.

Become a PLA Insider

Thank you for subscribing

Get exclusive insights, frameworks, and strategies from product leaders driving real business impact.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn